- Do you know the benefits associated with Traditional Financing?Conventional loans offer aggressive prices, flexible terms favorable link and conditions, and you can use of. Which have standard recommendations, it suit varied financial desires, while making homeownership possible and cost-productive. The ability to modify down money enhances independence, bringing individuals that have a personalized and you can positive credit feel.

- The length of time does it take to become approved to own a traditional Loan?Brand new acceptance processes for a traditional Loan can vary anywhere between lenders, it often takes 29 so you’re able to forty five weeks. Other variables one to determine the rate of your own process are papers completeness, property assessment, and you will bank overall performance dictate the latest schedule. A proper-prepared application expedites approval, but differing things could affect the course.

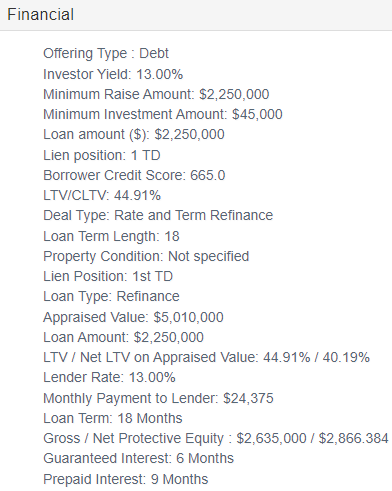

- Do i need to use a normal Mortgage having refinancing?Yes, you need a traditional loan to possess refinancing. Whether you are seeking lower pricing, modifying words, or opening equity, they provide a streamlined option for your position. The standard advice and you will greater lender anticipate ensures that you could appreciate an easier capital process.

- Just what credit history offers me an informed costs and terms getting a conventional Mortgage?To discover the best rates and you will conditions to your a conventional financing, choose a credit rating more than 720. Highest results denote straight down risk in order to lenders, unlocking much more good interest rates and you may words, sooner reducing the overall cost out-of credit. Maintaining excellent credit advances your capability so you can safer optimum financial support criteria.

- Is actually present money desired into down payment?Yes, conventional fund have a tendency to allow present money into the down payment. Family or accredited offer also provide this economic gift, facilitating homeownership. Obvious files is very important to verify the brand new gift’s authenticity and you can compliance that have lender guidelines.

- How many times is actually financing limits updated?Mortgage limitations having antique loans was analyzed a year. New Government Construction Finance Agency (FHFA) assesses business trends and you may adjusts limits so you’re able to reflect alterations in construction rates. Becoming informed about this type of condition is crucial having consumers to make sure their amount borrowed aligns into the newest restrictions in their certain area.

- Could there be an initial-day homebuyer importance of Old-fashioned Loans?Antique fund do not strictly has actually a primary-big date homebuyer requisite. not, first-go out consumers can benefit away from software such as HomeReady and you may House You can, providing lower down repayments and flexible terms and conditions. One debtor, despite homeownership records, is be eligible for a traditional Mortgage based on basic standards.

What’s the difference between a home loan Banker and you may a large financial company?

Home financing banker and you can a large financial company are both experts who let some one receive money to buy a residential property, however, there are a few key differences between the 2. Consequently the mortgage banker is in charge of underwriting new financing and you may offering the money for the borrower to utilize so you’re able to buy a house. However, a large financial company is actually an effective middleman exactly who works with several lenders to simply help consumers find a very good financing due to their needs. A mortgage broker does not supply the loans to your financing individually, but rather helps brand new debtor discover a lender and you can facilitate the borrowed funds app processes getting a charge.

What is actually home financing Banker?

As a result the borrowed funds banker is responsible for underwriting the brand new loan and you will offering the finance into the borrower to utilize so you’re able to purchase property. A mortgage banker may work with a big standard bank, particularly a financial, or may be an independent organization one focuses on getting household money. The borrowed funds banker is in charge of evaluating the fresh new borrower’s finances and you can credit history so you’re able to dictate their ability to settle the borrowed funds, and also will work with this new debtor to determine the top financing equipment and you can conditions for their demands. Occasionally, home financing banker may provide other economic attributes, such suggestions about to get property or refinancing a current mortgage.