- New borrower should individual no less than fifteen% to help you 20% of the property is thought the right candidate for an excellent domestic security loan.

- The latest shared financing-to-well worth proportion of the home should not go beyond 80%.

- This new borrower’s personal debt-to-income proportion shall be lower than 43%.

- The very least credit score of 620 can be called for.

- The property which will be used as guarantee should be appraised by the an authorized that’s acknowledged or appointed by the financial institution.

Payment regarding Family Equity Funds

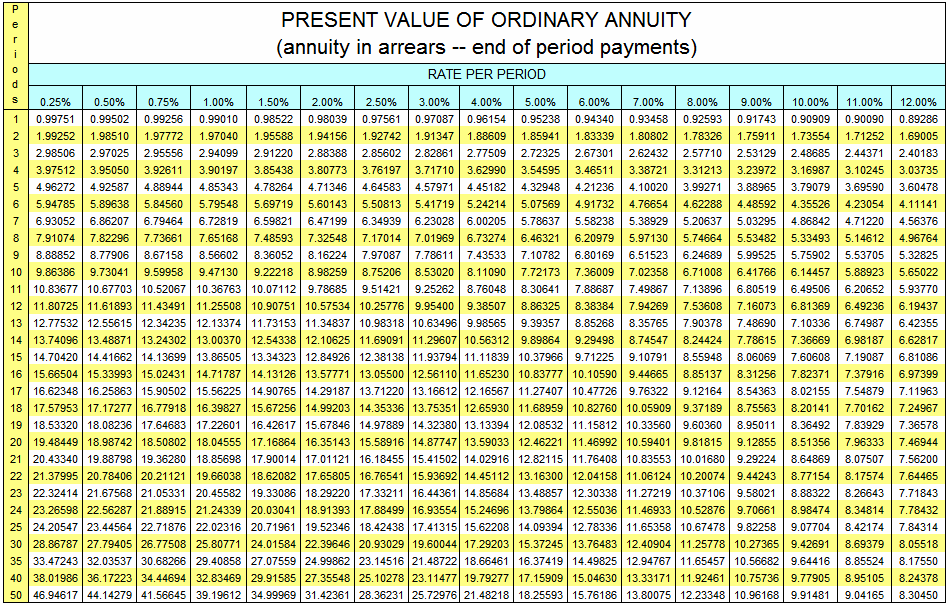

Domestic security funds is approved as a lump sum, in addition they are used for various intentions. Such funds is paid off as a result of some installments that always offer out of 10 to twenty five years.

For every single cost include an element of the loan’s a fantastic harmony and you will an appeal charge reduced towards lender because settlement to possess facilitating the funds. As for every single cost is reduced, the latest citizen more and more recoups part of the residence’s security.

Just before 2017, the interest charge paid down to the household security financing was indeed completely allowable out-of another person’s taxation. It improved the latest interest in this type of money since they was in fact a inexpensive replacement for other sorts of individual finance.

Nevertheless, the fresh Income tax Slices and you may Employment Acts out of 2017 got rid of the possibility of deducting the eye paid off in these fund with the exception of affairs where fund are widely used to get, build, or enhance the taxpayer’s household.

It modification decreased the fresh new appeal of family security fund, as they are nevertheless a nice-looking option due to the all the way down interest recharged for the household equity financing compared to private money.

Foreclosure down to Defaulted Family Security Financing

Given that a house security mortgage works because home financing, the underlying possessions serves as guarantee in case your borrower fails to satisfy their obligations. As a result lenders feel the right to foreclose towards the family, even though they can choose to not ever significantly less than particular things.

Such as for example, in case your worth of the mortgage is significantly less than the newest value of the house or property, the financial institution will most likely want to foreclose toward home. There can be a high possibility that they’ll receive adequate money from offering the property to fund to the an excellent balance of financial obligation.

As well, in case your worth of the home provides refuted that is now less than the brand new a good harmony of the financial obligation, the lender will get choose never to foreclose your house because will likely bring about an economic loss. Nevertheless, the financial institution you’ll still document an appropriate claim up against the borrower, which could sooner apply at their borrowing from the bank problem.

Home Guarantee Fund & Credit scores

A good borrower’s fee background with the a home collateral mortgage may affect the credit history. Such finance are addressed due to the fact an everyday borrowing account, and any later money will adversely perception another person’s borrowing problem.

Household Equity Finance versus. Family Security Credit lines (HELOCs)

Home guarantee credit lines (HELOCs) are experienced a second financial, nonetheless work differently than simply domestic collateral finance as they are rotating credit profile. This is why rather than a lump sum payment, HELOCs allow the debtor to help you withdraw money from the financing membership and you may pay-off the bill any kind of time considering area in the mark period.

- Availability of the income: Property security loan usually contains the debtor which have a lump contribution percentage for the whole level of the borrowed funds, when you find yourself an excellent HELOC functions much like a credit card. The new debtor takes currency out of the credit line on one section in draw months and pay it back while they excite. Given that draw months ends, don’t distributions can be made, and also the debtor must pay straight back new loan’s principal, and the focus fees applicable in the fees stage.